")

College Admissions with Calm, Clarity & Confidence

the blog

read post

Typically the first question families ask after their kid gets an offer of college admission is: How much will this cost? Unfortunately, there is no uniform format for delivering financial aid offers. And some colleges have confusing ways of labeling grants, scholarships, and loans. So understanding college financial aid offers takes time and attention to […]

Read More

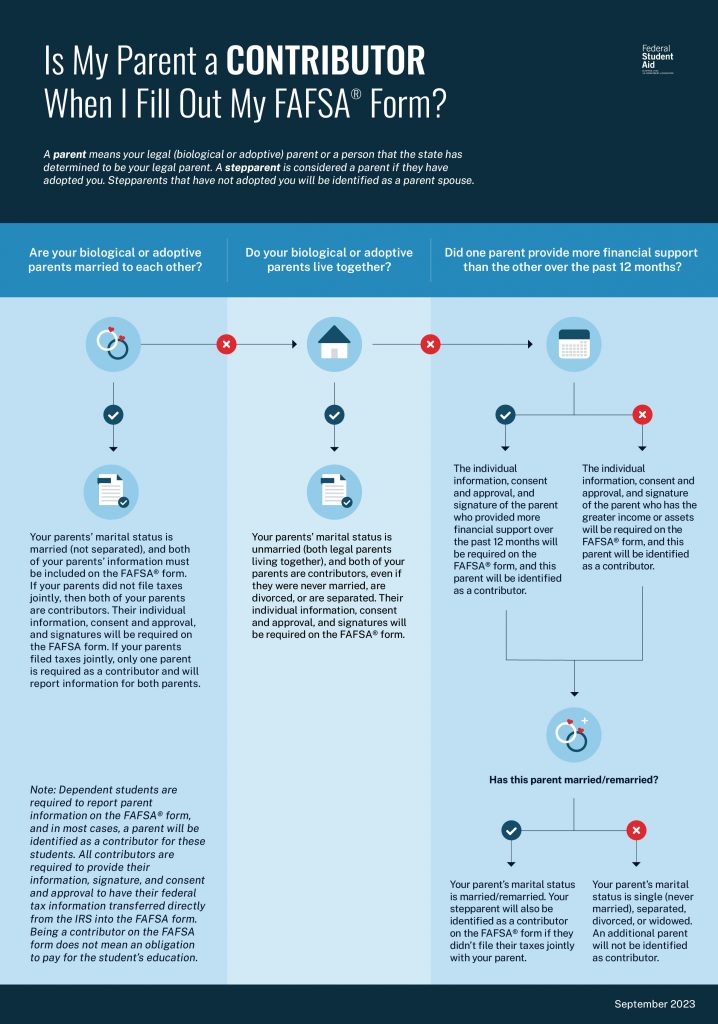

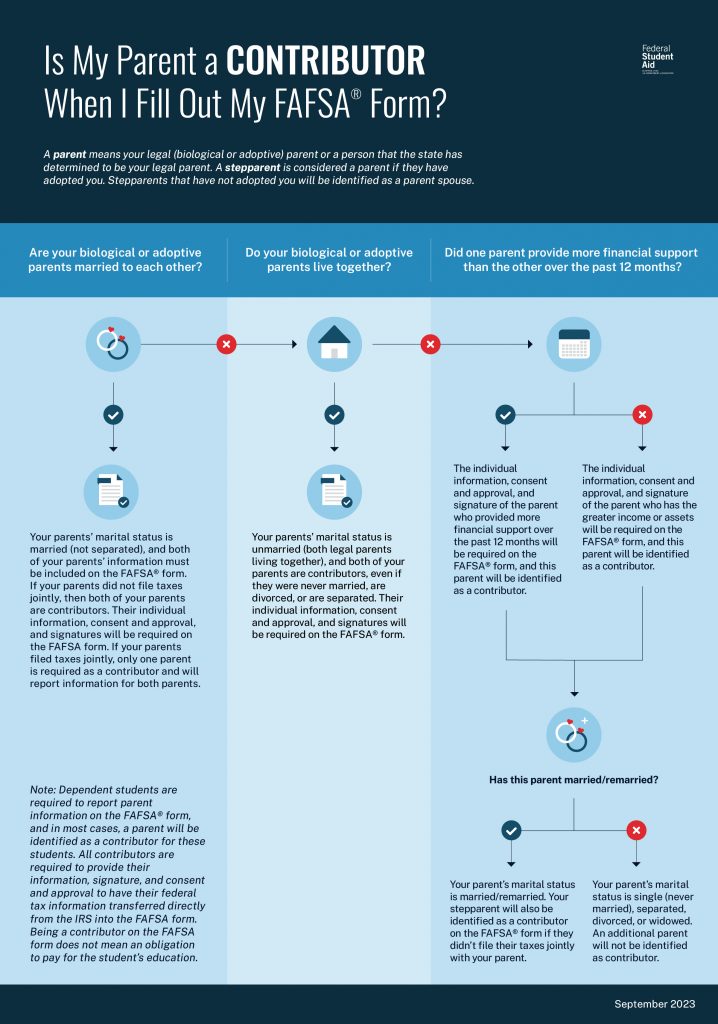

Recent FAFSA revisions introduced the term Contributor to refer to anyone other than the student who has to submit financial information for the application. This shift in terminology, combined with misunderstandings about what makes an independent student, and changes to which parent responds if they are unmarried has caused some confusion over the parent role […]

Read More

Did you know that when you apply to college can affect how much money you end up paying? Students often focus on whether or not they should apply under a binding Early Decision option, but overlook how applying later in the cycle can limit their chances of receiving certain types of financial aid. Some colleges […]

Read More

How the FY26 Budget Bill (HR1) could affect college financial aid is a question many families should be asking right now. The FY26 budget bill recently passed by the House of Representatives (known as HR1, or One Big Beautiful Bill Act) includes several proposed changes that could significantly affect how students and parents pay for […]

Read More

If you’re finishing junior year, use the summer to get a head start on college applications. With steady work over the next few months, you could be ready to submit applications shortly after they open in August, well before early application deadlines. Here’s what to work on before school ends and during the summer. Before […]

Read More

The Department of Education announced on November 14, 2024 that the FAFSA 2025-26 is available to all students through the Beta test version. This means any students can apply for federal financial aid for the 2025-26 college academic year through the Free Application for Federal Student Aid (FAFSA). Students and their “contributors” (aka parents submitting […]

Read More

College affordability matters. Understanding college costs and financial aid works should be one of your first steps in making a college list. This is a long article, but I want to give you a strong overview of college costs and financial aid, so you are prepared to consider your options. Think about your family budget, college […]

Read More

If you have a high school student, maybe you’ve noticed articles about FAFSA. Maybe you’re worried about completing it so you can get a financial aid offer. Maybe you are just wondering, “What is FAFSA?” This guide explains what FAFSA is, why it matters, and where to get help completing it. As of January 2024, […]

Read More

FAFSA is the Free Application for Federal Student Aid. FAFSA 2024-25 (for the college academic year that starts in Fall 2024) opened December 31, 2023 in a soft launch. This revised form reflects changes to the format and the formula used to calculate eligibility for need-based financial aid. These FAFSA tips will help you finish […]